The Business of Fashion

Agenda-setting intelligence, analysis and advice for the global fashion community.

Agenda-setting intelligence, analysis and advice for the global fashion community.

When fashion tastemakers file into the Revolve Gallery during New York Fashion Week, the online retailer expects that splashy displays by labels like Aya Muse, Kim Shui and Michael Costello will inspire them to snap up hundreds of thousands of dollars in merchandise.

For Revolve, what they don’t see is equally important.

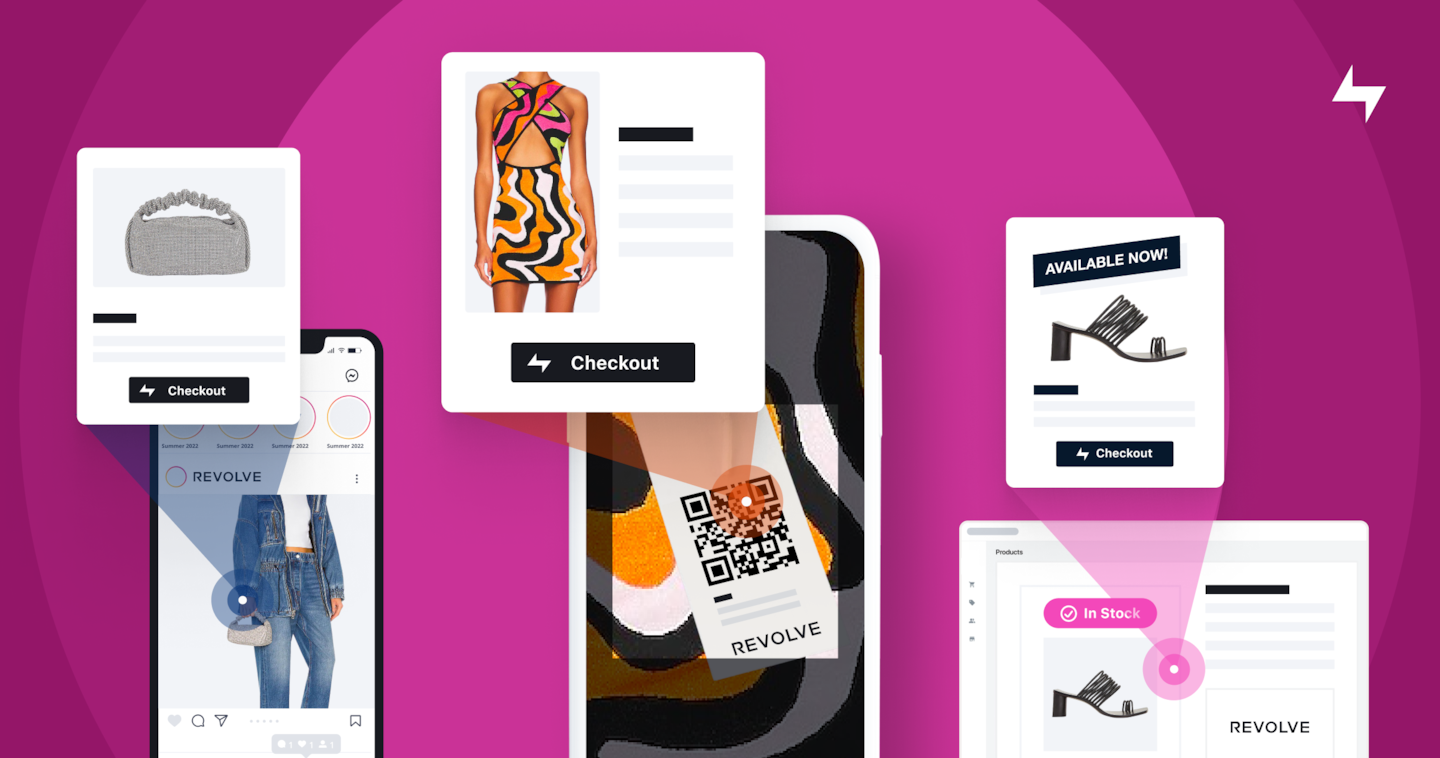

The installation is doubling as the debut of a new checkout process, a product created by technology service provider Bolt, where QR codes on clothing tags direct customers to the retailer’s website to complete their purchases with one click. The hope is shoppers will find the process easier to navigate, increasing the odds they complete their purchase. And crucially, they’ll bypass the crowded checkout pages — with tempting logos for “buy-now, pay-later” services — that have become increasingly common on retail websites.

Over the last three years, instalment payment services became ubiquitous on fashion retailers’ checkout pages. Buy now pay later brought in new customers, who spent more knowing they could spread out payments over weeks or months.

ADVERTISEMENT

Some retailers are having second thoughts about that relationship, however. Klarna, Affirm and Afterpay have seen valuations plummet amid new regulations and rising borrowing costs. These concerns have been amplified as the fintech firms have sought to become consumer brands themselves. The biggest advertise heavily (Afterpay is the lead sponsor of New York Fashion Week as well as London Fashion Week under its UK subsidiary, Clearpay).

In fashion, companies are nervous about allowing yet another intermediary to have dibs on data about their customers and transactions — similar concerns have kept many brands off of Amazon and other e-commerce sites.

“We may not have been willing to partner with Bolt if they hadn’t been so flexible with us in terms of being able to access the data that we felt like we needed to access and own the data that we felt like we needed to own,” said Revolve co-chief executive and co-founder Mike Karanikolas.

Trade Off

Retailers have always relied on outside companies to handle complicated back-office functions, such as logistics. But with the rise of e-commerce, services firms have become more involved in the customer relationship, with BNPL as the latest example. The benefits are obvious, the costs sometimes only become clear later, said Hemal Nagarsheth, partner in the financial services practise at business consultancy Kearney.

“BNPL partnerships can get you access to capabilities around things like technology and a seamless checkout experience — which are super important,” Nagarsheth said. “The question that some retailers have not had a chance to discuss … is how to treat that relationship and what data should and shouldn’t get shared.”

For instance, when a consumer opts to check out with Afterpay, they are taken to the BNPL firm’s website to complete the transaction. Afterpay — or Klarna, Affirm, or most other instalment plan companies — may then own valuable information about who that customer is, as well as broader data on shopping habits. They can use this data to develop relationships of their own with consumers — Klarna even has a “super app” where customers can browse retailers’ websites and make purchases without leaving the fintech firm’s ecosystem.

“There’s this idea that retail is at the centre of everything that the consumer does,” said Deborah Weinswig, the founder and chief executive of Coresight Research. “I think in some ways, many consumers feel much better about that as opposed to solution providers having all [their] data.”

ADVERTISEMENT

From Frictionless to Invisible

What many fashion companies now want from third party vendors is the frictionless solutions they promise all while staying invisible, experts say.

“The future is to keep lowering friction, make things really fast and really transparent,” said Keval Desai, a former Google executive and founder of SHAKTI, an early stage tech venture capital firm. “The more transactions you enable, the more money you make … instead of doing that, fintech companies have been doing all kinds of gymnastics.”

At its NFYW gallery, Revolve will also become the first to use Bolt’s latest product, Checkout Links, which allows shoppers to to check out with a single click wherever they discover a product, whether online (like in an email or blog post from a brand) or offline (such as at a NYFW pop-up, a trade show or in a store.)

Revolve still offers BNPL options on its website, with Bolt acting as “a layer on top of all the different payment options,” giving the retailer access to more data, said Maju Kuruvilla, Bolt’s chief executive officer.

“Merchants are in this tough space where they’re trying to meet the customer where they are and the customers are using all these different alternate payment options,” said Kuruvilla. “But then, now that they’ve enabled all these options, merchants start [wondering] ‘who owns my customer and where is my data?’”

Even complementary solutions like Bolt aren’t without their kinks. In July, licensing company Authentic Brands Group settled a lawsuit against Bolt that alleged the online checkout service provider breached its contract and failed to deliver its payment software as promised and then changed the terms of their equity deal. As part of the settlement, ABG became shareholders of the fintech startup.

Like Bolt, other firms are looking for ways to offer BNPL-like services while leaving the retailer in charge of the customer relationship. Splitit, for example, allows consumers to turn large purchases into monthly instalments using their credit cards. It’s also a white label product, meaning Splitit’s branding stays behind the scenes and the customer is never re-routed to another website to complete their purchase.

ADVERTISEMENT

More traditional banks like Barclays and HSBC Bank, are also starting to build out buy-now pay-later options, as are credit card companies and payment processors such as Paypal. That can help allay consumer fears over privacy as well as help retailers avoid the added competition from BNPL start-ups, Nagarsheth said.

“For retailers, you would not consider a bank a competitor and, for consumers ... they trust banks with their data because banks hold their money,” he said.

It’s large retailers like Revolve that are in the best position to strike a different bargain with their service providers. Many smaller retailers are focused on acquiring more customers, and are willing to sacrifice some control over the customer relationship to grow sales.

“The fight for consumer data is a very real fight,” said Nandan Sheth, chief executive of SplitIt.

The licensing company has settled and agreed to dismiss its case against Bolt, its e-commerce checkout service provider.

Revolve pioneered the concept of using influencer marketing to sell fashion. Now the retailer wants to use its network of social media stars to launch more brands of its own.

The buy now, pay later giant said it raised $800 million from new and existing investors, according to a statement Monday.

Sheena Butler-Young is Senior Correspondent at The Business of Fashion. She is based in New York and covers workplace, talent and issues surrounding diversity and inclusion.

Zero10 offers digital solutions through AR mirrors, leveraged in-store and in window displays, to brands like Tommy Hilfiger and Coach. Co-founder and CEO George Yashin discusses the latest advancements in AR and how fashion companies can leverage the technology to boost consumer experiences via retail touchpoints and brand experiences.

Four years ago, when the Trump administration threatened to ban TikTok in the US, its Chinese parent company ByteDance Ltd. worked out a preliminary deal to sell the short video app’s business. Not this time.

Brands are using them for design tasks, in their marketing, on their e-commerce sites and in augmented-reality experiences such as virtual try-on, with more applications still emerging.

Brands including LVMH’s Fred, TAG Heuer and Prada, whose lab-grown diamond supplier Snow speaks for the first time, have all unveiled products with man-made stones as they look to technology for new creative possibilities.